Let us cover the 12 financial regulators of India :

I. RBI

The Reserve Bank of India (RBI) is India’s central banking institution, which controls the monetary policy of the Indian rupee. It is the big daddy among all other regulators in India. It commenced its operations on 1 April 1935 during the British Rule in accordance with the provisions of the Reserve Bank of India Act, 1934. Following India’s independence on 15 August 1947, the RBI was nationalized on 1 January 1949. The general superintendence and direction of the RBI is entrusted with the 21-member Central Board of Directors: the Governor, 4 Deputy Governors, 2 Finance Ministry representatives, 10 government-nominated directors to represent important elements from India’s economy, and 4 directors to represent local boards headquartered at Mumbai, Kolkata, Chennai and New Delhi.

To read further, click here.

II. SEBI

The Securities and Exchange Board of India (SEBI) was established on April 12, 1992 in accordance with the provisions of the Securities and Exchange Board of India Act, 1992. The Preamble of the Securities and Exchange Board of India describes the basic functions of the Securities and Exchange Board of India as “…to protect the interests of investors in securities and to promote the development of, and to regulate the securities market and for matters connected therewith or incidental thereto”. It is headquartered in Mumbai. The current SEBI Chairman is U.K. Sinha.

To read further, click here.

FMC

Just as SEBI regulates the stock market, Forward Markets Commission (FMC) used to regulate the commodity market in India. It was established in 1953 under the provisions of the Forward Contracts (Regulation) Act, 1952 and was headquartered in Mumbai and this financial regulatory agency was overseen by the Ministry of Finance.

Let’s have a look at the history of commodity market in India. It should be noted that post independence, in the 1950s, India continued to struggle with feeding its population and the government increasingly restricting trading in food commodities. Just at the time the FMC was established, the government felt that derivative markets increased speculation which led to increased costs and price instabilities. And in 1953 finally prohibited options and futures trading altogether. The industry was pushed underground and the prohibition meant that development and expansion came to a halt. In the 1970 as futures and options markets began to develop in the rest of the world, Indian derivatives markets were left behind. The apprehensions about the role of speculation, particularly in the conditions of scarcity, prompted the Government to continue the prohibition well into the 1980s. The result of the period of prohibition left India with a large number of small and isolated regional futures markets. Next to the officially approved exchanges, there were also many havala markets. Most of these unofficial commodity exchanges have operated for many decades.

Since futures traded in India are traditionally on food commodities, the agency was originally overseen by Ministry of Consumer Affairs, Food and Public Distribution (India). In September 2013, the commission responsibility was moved to the Ministry of Finance to reflect that futures trading was becoming more and more a financial activity. FMC provided regulatory oversight in order to ensure financial integrity (i.e. to prevent systematic risk of default by one major operator or group of operators), market integrity (i.e. to ensure that futures prices are truly aligned with the prospective demand and supply conditions) and to protect & promote interest of consumers /non-members. Thus, it performed the role of a market regulator. After assessing the market situation and taking into account the recommendations made by the Board of Directors of the Commodity Exchange, the Commission used to approve the rules and regulations of the Exchange in accordance with which trading is to be conducted. It used to accord permission for commencement of trading in different contracts, monitor market conditions continuously and take remedial measures wherever necessary by imposing various regulatory measures. The commission appeared in the news in March 2012 for their ban on guar gum futures trading after it said the price quadrupled due to its use in fracking causing food inflation.

The Commission allowed commodity trading in 22 exchanges in India, of which 6 were national. The major national exchanges are (i) Multi-commodity Exchange of India Limited (MCX) Mumbai, (ii) National Commodity and Derivatives Exchange Limited(NCDEX), Mumbai and (iii) National Multi-commodity Exchange of India Limited(NMCE), Ahmedabad. However, subsequent to the passing of Finance Act 2015 and a notification to this effect, on 28 September 2015, the FMC was merged with the Securities and Exchange Board of India (SEBI). Thus FMC has now ceased to exist and the responsibility of regulating commodity markets have been given to the securities market regulator, SEBI. Mr. U.K. Sinha said the first priority would be to develop trust in the commodities market and then the focus would be on developing the market. The SEBI chief said that new participants like banks and FPIs (Foreign Portfolio Investors) as well as more products would be allowed.

III. IRDA

The Insurance Regulatory and Development Authority (IRDA) was constituted to regulate and develop insurance business and re-insurance business in India. As a key part of its role, the insurance regulator is responsible to protect the rights of policyholders. The current Chairman is T.S. Vijayan.

To read further, click here.

IV. PFRDA

The Pension Fund Regulatory and Development Authority (PFRDA) is a pension regulatory authority which was established by Government of India on August 23, 2003. PFRDA is authorized by Ministry of Finance, Department of Financial Services. The Union Parliament passed the IPRDA [Interim Pension Fund Regulatory & Development Authority] Bill in February 2003 as a Budget Announcement, approved by the then President of India, Dr. APJ Abdul Kalam. Tamil Nadu became the first state to implement NPS (National Pension Scheme) for its newly appointed employees from the financial year 2003–04, under the chief ministership of Jayalalitha. PFRDA promotes old age income security by establishing, developing and regulating pension funds and protects the interests of subscribers to schemes of pension funds and related matters. The Pension Fund Regulatory & Development Authority Act was passed on 19th September, 2013 to replaced the old PREDA Bill and the same was notified on 1st February, 2014, thus setting up PFRDA as the regulator for pension sector in India. However, there remains considerable amount of confusion with other entities like Employee Provident Fund, Pension funds run by Life Insurers and Mutual Fund companies being outside the purview of PFRDA. PFRDA is regulating the National Pension Scheme (NPS)*, subscribed by employees of Govt. of India, State Governments and by employees of private institutions/organizations & unorganized sectors. PFRDA is responsible for appointment of various intermediate agencies such as Central Record Keeping Agency (CRA), Pension Fund Managers, Custodian, NPS Trustee Bank, etc. The President of India is the Guardian of PFRDA of India, subject to his Financial Emergency Powers, as per the Articles of Indian Constitution. PFRDA now has Full Autonomy & functioning Independently from the F.Y. 2014-15. The present chairman of PFRDA is Hemant Contractor. PFRDA is head-quartered at New Delhi with various regional offices spread across the country.

*Comment: The National Pension System (NPS) is a voluntary defined contribution pension system administered and regulated by Pension Fund Regulatory and Development Authority (PFRDA) created by an Act of Parliament of India. It has its origins in the recommendations of the OASIS report, 1999. The NPS started with the decision of Government of India to stop defined benefit pensions for all its employees who joined after 1st Jan 2004. While the scheme was initially designed for government employees only, it was opened up for all citizens of India in 2009. NPS is an attempt by the government to create a pensioned society in India. In its overall structure NPS is closer to 401(k) plans of United States. NPS architecture consists of NPS Trust which is entrusted with safeguarding subscribers interests, a Central Recordkeeping Agency (CRA) which maintains the data and records and issues of PRAN or Permanent Retirement Account Number for customers who have availed savings plan under the National Pension Scheme, Point of Presence Agencies (PoPs) as collection, KYC verification and distribution arms, Pension fund managers (PFM) for managing the investments of subscribers, Custodian to take care of the assets purchased by the Fund managers and Trustee bank to manage the banking operations. At age 60 the customer can choose to purchase pension Annuity Service Providers (ASP). Apart from these there are Aggregators who can be understood as the most prominent and first point of contact between subscriber and the NPS – Swavalamban scheme as they are responsible for carrying out changes in any of the KYC information as requested by subscriber and also conduct grievance handling in cases where subscriber raises a complaint or grievance against any of the intermediaries of the PFRDA. Current CRA is National Security Depository Limited (NSDL). All the major commercial banks and brokers perform the role of PoP. The subscriber can choose anyone of them. There are 7 fund managers and 8 annuity service providers for subscribers to choose from. The subscriber can choose to invest either, wholly or in combination, 3 types of investment schemes offered by the Pension Fund Managers. These are Scheme E (Equity) which allows up to 75% equity participation, Scheme C (Corporate Debt) which invests only in high-quality corporate bonds, Scheme G (Government Bonds) which invest only in government bonds. Alternatively, the subscriber can opt for default scheme where as per the time left to retirement his portfolio is rebalanced each year for the proportion of Equity, Corporate Bond, and Government Bonds. A citizen of India, whether resident or non-resident can join NPS, if the resident’s age is between 18 – 60 years as on the date of submission of his/her application to the Point of Presence (PoP) / Point of Presence–Service Provider -Authorized branches of PoP for NPS (PoP-SP). The subscribers should also comply with the Know Your Customer (KYC) norms as detailed in the Subscriber Registration Form. Un-discharged insolvent and individuals of unsound mind cannot join NPS. NPS restricts withdrawals before the age of 60. As per latest regulations subscribers can make withdrawals from the scheme only after 10 years, only 3 times during the entire duration and at no point in time will withdrawals exceed the sum total of contributions made by the subscriber. NPS qualifies for tax benefits under three different sections of Indian tax laws- ⊗ Section 80C up to ₹ 150,000 ⊗ Section 80CCD(1) up to Rs 50,000 ⊗ Section 80CCD(2) up to 10% of basic salary contributed by the employer. All these tax breaks are independent of each other and can be availed simultaneously.

V. Ministry of Finance (MoF) and the Department of Financial Services (DFS)

The Ministry of Finance is an important ministry within the Government of India concerned with the economy of India. In particular, it concerns itself with taxation, financial legislation, financial institutions, capital markets, center and state finances, and the Union Budget.

The Department of Financial Services (DFS) of the MoF covers Banks, Insurance and Financial Services provided by various government agencies and private corporations. It also covers pension reforms and Industrial Finance and Micro, Small and Medium Enterprise. It started the Pradhan Mantri Jan Dhan Yojana in 2014.

PFRDA, Pension Fund Regulatory and Development Authority is a statutory body which also works under this department. The current minister of Finance is Arun Jaitley.

VI. Ministry of Corporate Affairs (MCA)

The Ministry of Corporate Affairs (MCA) is an Indian government ministry.The Ministry is primarily concerned with administration of the Companies Act 2013, the Companies Act 1956, the Limited Liability Partnership Act, 2008 & other allied Acts and rules & regulations framed there-under mainly for regulating the functioning of the corporate sector in accordance with law. It is responsible mainly for regulation of Indian enterprises in Industrial and Services sector. Note that Nidhi Companies and Mutual Benefit Companies are also regulated by it.The current minister of corporate affairs is Arun Jaitley.

EXTRA# VII. NABARD

National Bank for Agriculture and Rural Development (NABARD) was set up as an apex Development Bank with a mandate for facilitating credit flow for promotion and development of agriculture, small-scale industries, cottage and village industries, handicrafts and other rural crafts.It has the mandate to support all other allied economic activities in rural areas, promote integrated and sustainable rural development and secure prosperity of rural areas. NABARD regulates the institutions which provide financial help to the rural economy. It is the apex unit for deciding the policy for cooperative banks and the RRBs, and manages talent acquisition through IBPS CWE. It makes policies for the financial health of rural areas in accordance with the directions from RBI (RBI has 1% stake in it). Powers have been delegated to National Bank for Agricultural and Rural Development (NABARD) under Sec 35 A of the Banking Regulation Act (As Applicable to Cooperative Societies) to conduct inspection of State and Central Cooperative Banks.

The Committee to Review Arrangements for Institutional Credit for Agriculture and Rural Development (CRAFICARD), set up by the Reserve Bank of India (RBI) under the chairmanship of Shri B. Sivaraman, conceived and recommended the establishment of National Bank for Agriculture and Rural Development (NABARD). It was established on 12 July 1982 by a special act of parliament and its main focus was on upliftment of rural India by increasing the credit flow for elevation of agriculture & rural non farm sector and completed its 34 years on 1 Jan 2016. It is headquartered in Mumbai. The current chairman is Harsh Kumar Bhanwala.

To read further, click here.

EXTRA# VIII. FSDC

The Financial Stability and Development Council (FSDC) is an apex-level body constituted by the government of India. The idea to create such a super regulatory body was first mooted by the Raghuram Rajan Committee (Committee on Financial Sector Reforms, CSFR) in 2008. Finally in 2010, the then Finance Minister of India, Pranab Mukherjee, decided to set up such an autonomous body dealing with macro prudential and financial regularities in the entire financial sector of India. The recent global economic meltdown has put pressure on governments and institutions across the globe to regulate their economic assets. This council is seen as India’s initiative to be better conditioned to prevent such incidents in future. The new body envisages to strengthen and institutionalize the mechanism of maintaining financial stability, financial sector development, inter-regulatory coordination along with monitoring macro-prudential regulation of economy.

The Council has a Sub-committee headed by the Governor, RBl. The Sub-committee replaced the existing High Level Coordination Committee on Financial Markets. The Chairman of the FSDC is the Finance Minister of India (Arun Jaitley) and its other members include:

- The heads of the financial sector regulatory authorities (i.e, SEBI, IRDA, RBI and PFRDA) ,

- Finance Secretary (current: Ashok Lavasa) and/or

- Secretary, Department of Economic Affairs (Ministry of Finance) (current: Shaktikanta Das),

- Secretary, Department of Financial Services, Ministry of Finance (current: Ms Anjuly Chib Duggal), and

- The Chief Economic Adviser (current: Arvind Subramanian).

The commodities markets regulator, Forward Markets Commission (FMC) was added to the FSDC in December 2013 subsequent to shifting of administrative jurisdiction of commodities market regulation from Ministry of consumer Affairs to Ministry of Finance. Mandate: Without prejudice to the autonomy of regulators, this Council would monitor macro prudential supervision of the economy, including the functioning of large financial conglomerates. It will address inter-regulatory coordination issues and thus spur financial sector development. It will also focus on financial literacy and financial inclusion. What distinguishes FSDC from other such similarly situated organizations across the globe is the additional mandate given for development of financial sector.

EXTRA# IX. FIPB

The Foreign Investment Promotion Board (FIPB) was initially constituted under the Prime Minister’s Office (PMO) in the wake of the economic liberalization drive of the early 1990s. The Board was reconstituted in 1996 with transfer of the FIPB to Department of Industrial Policy and Promotion (DIPP). The FIPB was again transferred to the Department of Economic Affairs; Ministry of Finance. It is a national agency of Government of India, with the remit to consider and recommend foreign direct investment (FDI) which does not come under the automatic route. It is housed in the Department of Economic Affairs, Ministry of Finance, as an inter-ministerial body. The extant FDI Policy, Press Notes and other related notified guidelines formulated by Department of Industrial Policy and Promotion (DIPP) in the Ministry of Commerce and Industry are the bases of the FIPB decisions.

It provides a single window clearance for proposals on FDI in India. The sectors under automatic route do not require any prior approval from FIPB and are subject to only sectoral laws. Currently, The Minister of Finance who is in-charge of FIPB would consider the recommendations of FIPB on proposals with total foreign equity inflow of and below ₹ 3000 crore. The recommendations of FIPB on proposals with total foreign equity inflow of more than ₹ 3000 crore would be placed for consideration of Cabinet Committee on Economic Affairs (CCEA). The members of FIPB are:

- Secretary, Department of Economic Affairs – Chairman (current: Shaktikanta Das)

- Secretary, Department of Industrial Policy & Promotion – Member

- Secretary, Department of Commerce – Member

- Secretary, (Economic Relation), Ministry of External Affairs – Member

- Secretary, Ministry of Overseas Indian Affairs – Member

As per FDI Policy, 2015, Companies may not require fresh prior approval of the Government i.e. Minister-in-charge of FIPB/CCEA for bringing in additional foreign investment into the same entity, in the following cases:

(i) Entities the activities of which had earlier required prior approval of FIPB/CCFI/CCEA and which had, accordingly, earlier obtained prior approval of FIPB/CCFI/CCEA for their initial foreign investment but subsequently such activities/sectors have been placed under automatic route;

(ii) Entities the activities of which had sectoral caps earlier and which had, accordingly, earlier obtained prior approval of FIPB/CCFI/CCEA for their initial foreign investment but subsequently such caps were removed/increased and the activities placed under the automatic route; provided that such additional investment along with the initial/original investment does not exceed the sectoral caps; and

(iii) Additional foreign investment into the same entity where prior approval of FIPB/CCFI/CCEA had been obtained earlier for the initial/original foreign investment due to requirements of Press Note 18/1998 or Press Note 1 of 2005 and prior approval of the Government under the FDI policy is not required for any other reason/purpose.

(iv) Additional foreign investment into the same entity within an approved foreign equity percentage/or into a wholly owned subsidiary.

EXTRA# X. NHB

National Housing Bank (NHB), a wholly owned subsidiary of Reserve Bank of India (RBI) (which contributed the entire paid-up capital), was set up by an Act of Parliament – the National Housing Bank Act – in 1987. NHB is an apex financial institution for housing. It is headquartered in Delhi. The Preamble of the National Housing Bank Act, 1987 describes the basic functions of the NHB as –

“… to operate as a principal agency to promote housing finance institutions both at local and regional levels and to provide financial and other support to such institutions and for matters connected therewith or incidental thereto …”

It commenced its operations in 1988. National Housing Bank has been empowered to determine the policy and give directions to the housing finance institutions and their auditors to prevent the affairs of any housing finance institution being conducted in a manner detrimental to the interest of the depositors or in a manner prejudicial to the interest of the housing finance institutions. NHB registers, regulates and supervises Housing Finance Company (HFCs) registered under section 29A of the National Housing Bank Act, 1987, keeps surveillance through on-site & off-site mechanisms and co ordinates with other Regulators. Besides the regulatory provisions of the National Housing Bank Act, 1987, National Housing Bank has issued the Housing Finance Companies (NHB) Directions, 2001 as also Guidelines for Asset Liability Management System in Housing Finance Companies. These are periodically updated through issue of circulars and notifications. The present Capital Adequacy Ratio for NHB is ~18.5%. The current paid up capital is ₹1,450 crores.

The general superintendence, direction and management of the affairs and business of NHB vest, under the Act, in a Board of Directors. It has Shri Sriram Kalyanaraman as the Managing Director & Chief Executive Officer.

Some of the recent milestones of NHB over the years:

2000-2005

- First Residential Mortgage Backed Securitization Issue in the country

- Guidelines for Entry of HFCs into Insurance Business

- Credit Enhancement of Bonds floated by HFCs

- Liberalized Refinance Scheme for Housing Loans

- New Window of Lending to MFIs

- Capital Gain Bonds issued during this period – Capital gains arising from transfer of long-term capital assets (for example, any immovable property, jewellery/ precious metals or shares that have been held for 1 year) can be invested in these bonds within a period of 6 months from the date of transfer of the asset for getting exemption from the capital gains tax under Section 54 EC of Income Tax Act, 1961.

Note: Capital Gain Bonds are issued by SIDBI, NHB, NHAI and REC.

2005-2010

- Fraud Management Cell set up to disseminate information on frauds committed on housing loans

- NHB RESIDEX launched (First Official Residential Housing Price Index – The index has been constructed using the weighted average methodology with Price Relative Method [Modified Laspeyres approach] with the data on housing prices obtained from Central Registry of Securitisation Asset Reconstruction and Security Interest of India (CERSAI), the central online mortgage registry of India, for computation of the indices)

- Reverse Mortgage Loan for Senior Citizens (Reverse Mortgage is a financial product that enables senior citizens (60 +) who own a house to mortgage their property with a lender and convert part of the home equity into tax-free income without having to sell the house; maximum period of loan being twenty years and on the borrower’s death, the loan is repaid through sale of property)

- Refinance for Top-up Loan for Indira Awas Yojana Beneficiaries

- Equity participation in New Rural Housing Finance Companies

- Rural Housing Microfinance Launched

- NHB_UNESCAP study on pro-poor housing finance: 7 Asian Countries initiated

- Home Loan Counseling : Diploma programme put in place (IIBF)

- Creation of Rural Housing Fund with 2000 Crores Allocation

- Designated as Nodal Agency for implementing the Government of India’s Interest Subsidy Scheme for Housing the Urban Poor (ISHUP)

- Initiated joint study with KFW Germany regarding feasibility of developing energy efficient housing including financing

- NHB has financed a Mass Housing Project of the Government of West Bengal for EWS/LIG segments through Public Private Partnership to provide low income housing for the poor

- NHB Suvriddhi (Tax Saving) Term Deposit Scheme, 2008 and NHB Sunidhi term deposit scheme, 2008 – Under the Suvriddhi scheme, deposits (₹ 10,000 – ₹ 1,00,000) made by resident individuals and HUFs get Section 80C benefit. The deposit under this scheme will have lock-in period of 60 months. Sunidhi scheme, on the other hand, is a term deposit scheme (minimum deposit ₹ 50,000) for Individuals/ HUFs/ Partnerships/ Societies & Trusts & Association of persons. While the interest rates offered on Sunidhi term deposits is 7.25% compounded quarterly for 12 months/24 months and 7.50% compounded quarterly for 36 months/60 months, the interest rate on Suvridhi is 7.50% compounded quarterly. Senior citizens get an additional rate of 0.60% p.a. (as of Sept, 2016) on each scheme.

2010-2012

- SKOCH Financial Inclusion Award 2011 for its intervention in rural housing

- Collaboration with Kfw, Germany for promotion of Energy Efficient Housing 2011-2012 (Energy Efficient Housing Scheme)

- NHB-RESIDEX expanded from January 2012 to cover 5 new cities taking the total number of cities to 20

- Credit Risk Guarantee Fund Trust for Low Income Housing (CRGFTLIH) set up

- The SKOCH Financial Inclusion Awards – 2012 for project in Energy Efficient New Residential Housing in India.

EXTRA# XI. State Governments

Chit Fund Companies are regulated by the respective State Governments. Besides, every State/ UT Government have been requested to set up a State Level Coordination Committee (SLCC) for effective implementation of the central government schemes and monitoring of the unauthorised collection of deposits. As all the relevant financial sector regulators and enforcement agencies participate in the SLCC, it is possible to quickly share the information and agree on an effective course of action to be taken against entities indulging in unauthorized and suspect businesses involving funds mobilization from public. The SLCC is chaired by the Chief Secretary / Administrator of the concerned State/UT and has, as its members, apart from the Reserve Bank, the Regional Directorate of the MCA/ ROC, local unit of SEBI, NHB, Registrar of Chits, ICAI, Economic Intelligence Unit of the State Police and officials from Law and Home Ministries of the State Government.

Note that, if NBFCs associate themselves with proprietorship/ partnership firms accepting deposits in contravention of RBI Act, they are also liable to be prosecuted under criminal law or under the Protection of Interest of Depositors (in Financial Establishments) Act, if passed by the State Governments. It empowers the State Governments to take action even before the default takes place or complaints are received from depositors.

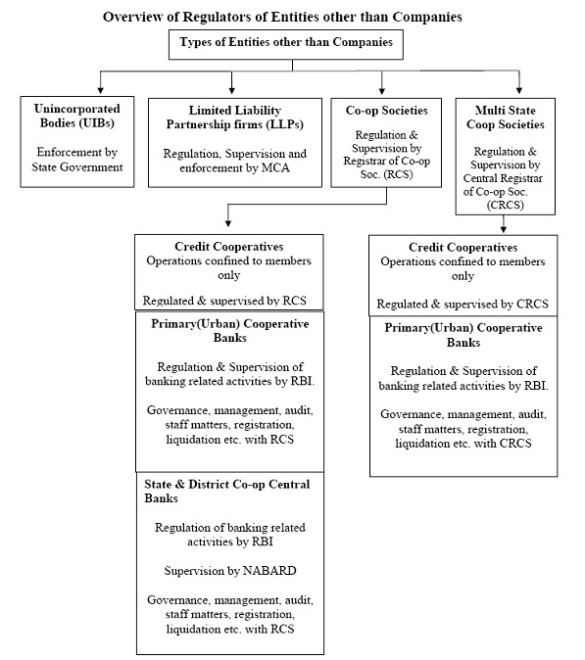

EXTRA# XII. Registrars of Co-operative Societies (RCS and CRCS)

In terms of the Cooperative Societies Acts of respective States, the Registrar of Co-operative Societies (RCS) was the sole regulator and supervisor of all the societies registered in his State including societies carrying on banking business. With the application of Banking Regulation Act, 1949 to cooperative societies carrying on banking business this position changed. The Reserve Bank became the regulator and supervisor of banking activities carried on by cooperative societies. In terms of the Cooperative Societies Act of the State, the Registrar of Cooperative Societies was to have jurisdiction over the incorporation, registration, management, amalgamation, merger, liquidation etc. and the Reserve Bank was to have jurisdiction over the banking activities of the cooperative society. The Reserve Bank regulates the banking functions of State Co- operative Banks (StCBs), District Central Co-operative Banks (DCCBs) and Urban Cooperative Banks (UCBs) under the provisions of Sections 22 and 23 of the Banking Regulation Act, 1949 (As Applicable to Cooperative Societies (AACS). Thus, there is a duality of control over these banks with banking related functions being regulated by the Reserve Bank and management related functions regulated by respective State Governments/ Central Government.

At the central level, The Office of Central Registrar of Cooperative Societies (CRCS) functioning under the Department of Agriculture & Cooperation, Ministry of Agriculture, handles the work of registration and management of multi state cooperative societies.

Currently, the Reserve Bank acts in close co-ordination with other regulators, such as, Registrar of Co-operative Societies and Central Registrar of Co-operative Societies. The Reserve Bank enters into Memorandum of Understanding (MoU) with Central Government and all State Governments which have presence of UCBs to ensure greater convergence of policies on regulation and supervision. Starting with signing first MoU with the State of Andhra Pradesh on June 27, 2005 and the last with the State of Telangana on December 30, 2014, today, all the UCBs in the country are covered under MoU. As part of the arrangements under MoU, the Reserve Bank constitutes a State-level Task Force for Co-operative Urban Banks (TAFCUB) for UCBs which operate only in one State. TAFCUBs bring all the decision-makers with regard to UCBs on one table, thus facilitating quick decision-making.

That’s all folks.